Articles

Unlocking Africa’s SME Potential through Digitalization

Jean Elie N’Goran

Nov 7, 2025

6 Min Read

Small and medium enterprises (SMEs) are the backbone of Africa’s economies, representing over 90% of businesses and 70% of jobs. Digitalization can be their most powerful growth lever unlocking productivity, transparency, and access to markets.

From Mobile Money to a New Financial Era

Africa stands at the forefront of a global financial transformation. Over the past decade, the continent has achieved what few thought possible: bringing hundreds of millions of people into the financial system through mobile money. Yet, this first digital leap was only the beginning.

Today, a second wave Fintech 2.0 is rising. It goes beyond basic transactions, integrating savings, credit, insurance, and investments into digital platforms. This shift represents not just technological progress, but an opportunity to reshape Africa’s competitiveness, empower small businesses, and strengthen resilience.

Recent data show that Africa counts over 540 active fintech companies, generating more than 150,000 direct jobs and billions in annual value creation. Countries such as Senegal, Côte d’Ivoire, and Morocco are emerging as regional leaders, connecting innovation with regulation and inclusion.

I. Diagnosis – Ten Years That Changed Everything

A mobile revolution that redefined access

In less than a decade, mobile money turned Africa into a global benchmark for digital inclusion. More than 1.1 billion registered accounts now process over $1.3 trillion in annual transactions about 45% of Africa’s GDP.

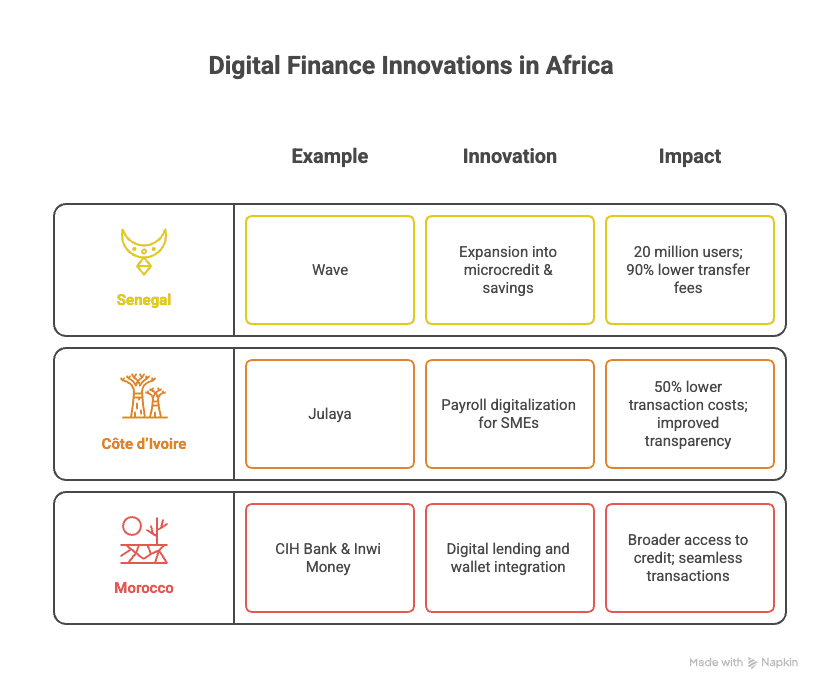

Platforms such as M-Pesa, MTN MoMo, and Wave proved that inclusion can be profitable. In Senegal, Wave has reduced transfer fees by 90%, reaching more than 20 million users across West Africa.

However, 75% of these users still rely solely on payment services, with limited access to credit, savings, or insurance the deeper layers of inclusion

Fragmented ecosystems and uneven regulation

Despite progress, interoperability remains a challenge. Most African central banks manage separate digital finance frameworks, complicating cross-border transactions.

For example, a user in Senegal cannot yet use the same wallet in Côte d’Ivoire or Morocco. This fragmentation hinders scale though initiatives like the AfCFTA Digital Payment and Settlement Platform (DPSP), launched in 2023, aim to unify standards across Africa.

Funding and sustainability gaps

In less than a decade, mobile money turned Africa into a global benchmark for digital inclusion. More than 1.1 billion registered accounts now process over $1.3 trillion in annual transactions about 45% of Africa’s GDP.

Platforms such as M-Pesa, MTN MoMo, and Wave proved that inclusion can be profitable. In Senegal, Wave has reduced transfer fees by 90%, reaching more than 20 million users across West Africa.

However, 75% of these users still rely solely on payment services, with limited access to credit, savings, or insurance the deeper layers of inclusion.

II. Strategic Levers – From Payments to Platforms

Expanding financial ecosystems

Fintech 2.0 is about integration. Leading companies are diversifying beyond transfers to become multi-service financial platforms:

Credit and micro-lending tailored to informal workers and SMEs.

Savings and micro-insurance integrated into mobile wallets.

Investment tools offering access to local capital markets.

In Côte d’Ivoire, Julaya enables SMEs to digitize payroll and supplier payments, cutting transaction costs by 50%. In Morocco, CIH Bank’s Digital Lab and Inwi Money are piloting digital credit services under regulatory supervision.

Data as the new financial infrastructure

With over 60% of Africans lacking a traditional credit history, data analytics becomes the foundation of inclusion. By analyzing payment patterns, telecom activity, and transaction histories, fintechs can generate alternative credit scores, unlocking access to finance for millions.

This data-driven model transforms inclusion into competitiveness allowing SMEs, farmers, and micro-entrepreneurs to prove their reliability in real time. Côte d’Ivoire’s 2024 Digital Identity Program (e-ID), for instance, will integrate KYC verification across all fintechs to improve security and reduce onboarding costs.

Collaboration and trust buildig

The fintech ecosystem thrives where collaboration replaces competition. Governments and innovators must work together to design stable, transparent frameworks that ensure trust.

Senegal’s Digital Financial Services Observatory monitors market transparency and consumer protection. In Morocco, the national payment switch (GIM) now connects with fintech APIs, facilitating real-time interoperability between banks, wallets, and payment processors.

Such initiatives lay the foundation for an inclusive, harmonized financial market, essential for continental integration.

III. Case Studies - The Fintech 2.0 Momentum

These examples reflect the broader transition from transactional fintech to ecosystem fintech where technology, regulation, and trust converge to reshape Africa’s economic landscape.

IV. Outlook - Inclusion as a Competitive Advantage

The evolution toward Fintech 2.0 goes beyond innovation; it’s about sovereignty and growth.By 2030, digital finance could add $200 billion to Africa’s GDP and generate 3 million new jobs.

Three strategic outcomes stand out:

Competitiveness: Digital finance lowers costs and accelerates productivity, particularly for SMEs.

Inclusion: By extending credit and insurance, fintech empowers vulnerable groups and boosts resilience.

Integration: A harmonized fintech market strengthens intra-African trade under the AfCFTA framework.

The challenge for policymakers and private actors is to ensure that this new ecosystem remains secure, interoperable, and equitable a foundation for the Africa of tomorrow.

Conclusion - Building the Next Financial Architecture

Africa’s fintech success story is only beginning. The continent now has the talent, data, and ambition to build its own financial infrastructure one that is inclusive, digital, and distinctly African.

To achieve that vision, three imperatives emerge:

Scale connectivity and infrastructure to sustain interoperability across borders.

Invest in trust and cybersecurity, the foundation of user confidence.

Promote sustainable capital and partnerships that empower startups and protect consumers.

Fintech 2.0 is not about disruption; it’s about transformation with purpose creating value that endures, strengthens economies, and ensures that inclusion becomes Africa’s greatest competitive advantage.

Join our newsletter list

Sign up to get the most recent blog articles in your email every week.

Author

Jean Elie N’Goran

Jean Elie N’Goran is a strategy and public policy expert with 10+ years of experience across Africa. Known for his clear, pragmatic approach, he helps organizations turn complex challenges into actionable growth strategies. Passionate about innovation, he shares insights that make transformation simple, data-driven, and impactful.